Mitigation Actions for Homeowners

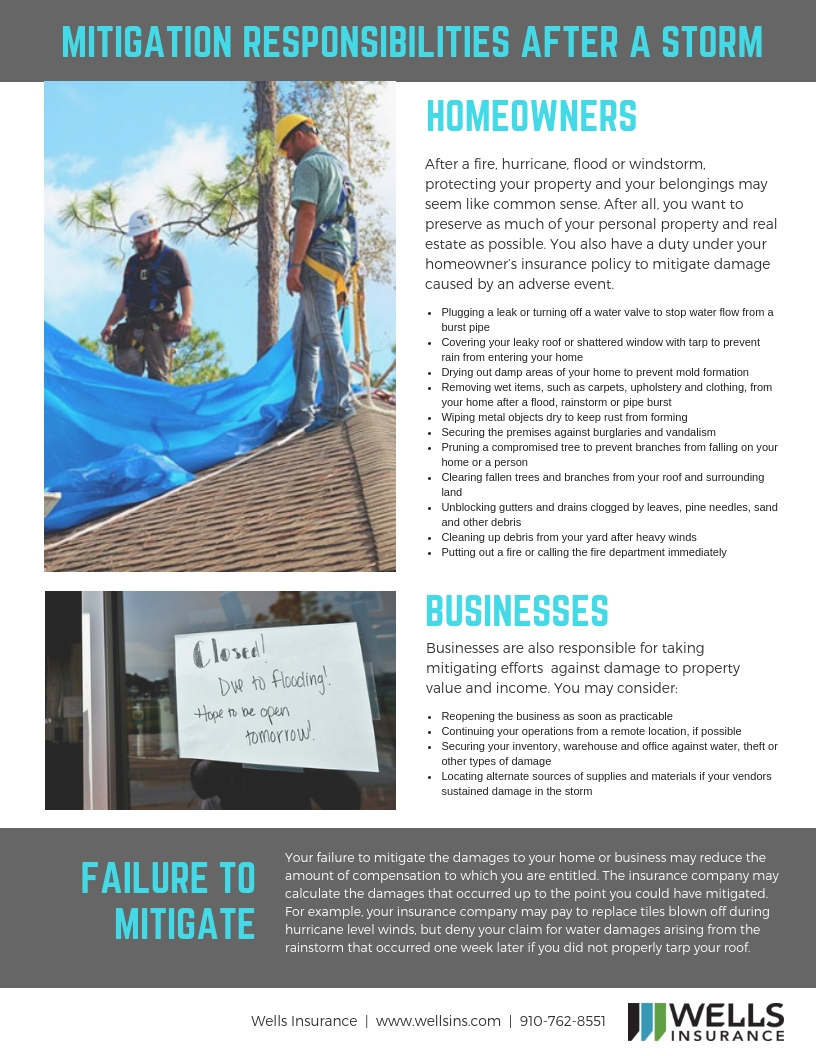

After a fire, hurricane, flood or windstorm, protecting your property and your belongings may seem like common sense. After all, you want to preserve as much of your personal property and real estate as possible. You also have a duty under your homeowner’s insurance policy to mitigate damage caused by an adverse event. Examples of mitigation include:

· Plugging a leak or turning off a water valve to stop water flow from a burst pipe

· Covering your leaky roof or shattered window with tarp to prevent rain from entering your home

· Drying out damp areas of your home to prevent mold formation

· Removing wet items, such as carpets, upholstery and clothing, from your home after a flood, rainstorm or pipe burst

· Wiping metal objects dry to keep rust from forming

· Securing the premises against burglaries and vandalism

· Pruning a compromised tree to prevent branches from falling on your home or a person

· Clearing fallen trees and branches from your roof and surrounding land

· Unblocking gutters and drains clogged by leaves, pine needles, sand and other debris

· Cleaning up debris from your yard after heavy winds

· Putting out a fire or calling the fire department immediately

While you should do everything within your power to minimize damage, you are not expected to put yourself in harm’s way to mitigate damages. Take efforts to mitigate only after your safety is assured.

You are also not expected to take action that is beyond your ability or skill level, such as removing heavy debris. In such a situation, you may need to contact a professional to assist you with your mitigation efforts.

Mitigation of Damage by Businesses

Businesses are also responsible for taking mitigating efforts against damage to property value and income. You may consider:

· Reopening the business as soon as practicable

· Continuing your operations from a remote location, if possible

· Securing your inventory, warehouse and office against water, theft or other types of damage

· Locating alternate sources of supplies and materials if your vendors sustained damage in the storm

Failure to Mitigate

Your failure to mitigate damages to your home or business may reduce the amount of compensation to which you are entitled. The insurance company may calculate the damages that occurred up to the point you could have mitigated. For example, your insurance company may pay to replace tiles blown off during hurricane level winds, but deny your claim for water damages arising from the rainstorm that occurred one week later if you did not properly tarp your roof.

Leave a reply